Profitability cases account for roughly 40% of all case interviews at McKinsey, BCG, and Bain. If you only have time to master one case type, this is it. The good news is that profitability cases follow a fairly predictable diagnostic pattern. The bad news is that interviewers know this, so they are looking for depth, nuance, and business judgment – not just a formulaic walkthrough.

The Profitability Equation

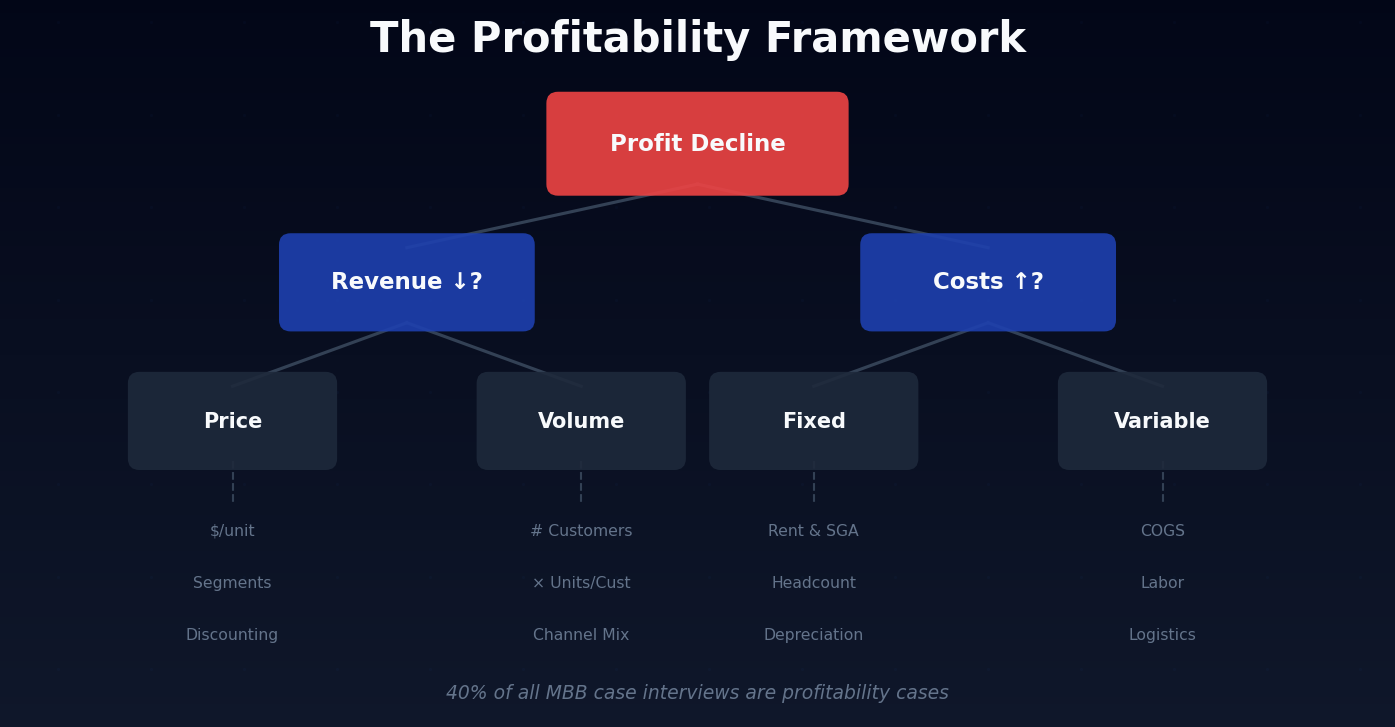

Every profitability case starts with the same fundamental equation:

Profit = Revenue - Costs

This breaks down further:

- Revenue = Price x Volume (units sold)

- Costs = Fixed Costs + Variable Costs

Your first job is to figure out which side of the equation is causing the problem. Is revenue declining? Are costs increasing? Or both? This sounds simple, but many candidates skip this diagnostic step and start brainstorming solutions before they understand the root cause.

Step 1: Isolate the Problem

When the interviewer tells you that a company’s profits have declined, your first question should be about the trend. Ask something like:

- “Has this decline been gradual over several years, or was there a sudden drop?”

- “Is this affecting the entire industry or just our client?”

These questions help you narrow the search. A sudden drop suggests a specific event (lost a key customer, a cost shock, a pricing change). A gradual decline suggests structural issues (market shift, competitive pressure, cost creep).

Next, determine whether the issue is on the revenue side, the cost side, or both. You can ask the interviewer directly: “Do we know if revenue has been flat or declining, and has the cost base changed meaningfully?” Most interviewers will point you in the right direction.

Step 2: Drill Into Revenue

If the issue is revenue, you need to decompose it further. Revenue is Price times Volume, but in practice you should think about it across multiple dimensions:

By Product or Service Line

Does the client have multiple products? Is the decline concentrated in one line or spread across all of them? A company with three product lines where only one is declining has a very different problem than one where everything is shrinking.

By Customer Segment

Are all customer segments declining equally? Perhaps the enterprise segment is growing but the SMB segment is churning. Or perhaps one geography is underperforming. Segmenting revenue helps you find the specific pocket where the problem lives.

By Channel

Is the client selling through multiple channels (direct sales, online, distributors, retail)? Channel mix shifts can have enormous effects on both revenue and margin. A shift from direct sales to distributor sales, for instance, might maintain volume but reduce net revenue per unit.

Step 3: Drill Into Costs

If the issue is costs, break them into fixed and variable categories, and then get specific:

Fixed Costs

- Rent and facilities

- Salaried headcount

- Technology and infrastructure

- Insurance and overhead

Variable Costs

- Raw materials and COGS

- Hourly labor (production, fulfillment)

- Shipping and logistics

- Sales commissions

Ask yourself: have costs increased because of inflation (input costs went up), inefficiency (we are doing the same things less efficiently), or investment (we deliberately increased spending for growth)?

The distinction matters because each root cause implies a different recommendation. Inflation-driven cost increases might require pricing adjustments or supplier renegotiation. Inefficiency suggests operational improvements. Deliberate investment spending might be fine if it is generating future returns.

Step 4: Quantify the Impact

Once you have identified the root cause, quantify it. This is where many candidates fall short – they identify the right problem conceptually but never put a number on it. Interviewers love candidates who can do rough math on the fly.

For example, if you discover that raw material costs have increased 15% and materials are 40% of total costs, you can quickly calculate:

“If materials are 40% of our cost base and they increased 15%, that represents about a 6 percentage point hit to our margin. Given our client went from 22% to 9% margin, this explains roughly half of the 13-point decline. So there must be other factors at work as well.”

This kind of synthesis is what separates good candidates from great ones.

Step 5: Recommend and Prioritize

After diagnosing the problem, the interviewer will ask: “So what should the client do?” This is your moment to demonstrate business judgment. A strong recommendation has three characteristics:

- It directly addresses the root cause. If the problem is pricing, do not recommend a cost-cutting program.

- It is prioritized. Suggest two or three actions ranked by impact and feasibility, not a laundry list of ten ideas.

- It acknowledges trade-offs. Every recommendation has risks. Raising prices might lose price-sensitive customers. Cutting costs might affect quality. Acknowledging these shows maturity.

Common Traps in Profitability Cases

Watch out for these patterns that interviewers use to test your thinking:

- The “both sides” trap. Sometimes revenue is declining AND costs are rising. Do not assume it is only one.

- The segment trap. Overall revenue might be flat, but one segment is growing while another is shrinking. The net effect hides the real story.

- The investment trap. Costs are up because the company invested in a new product line. This is not necessarily a problem – you need to evaluate whether the investment will generate returns.

- The external factor. A new competitor entered the market, or regulation changed. These require different responses than internal operational issues.

How Caise Tests Profitability Skills

Knowing the framework is one thing. Performing under pressure is another. Caise has dozens of profitability cases spanning retail, healthcare, tech, manufacturing, logistics, and more – each designed to test whether you can actually execute the diagnostic pattern described above, not just recite it.

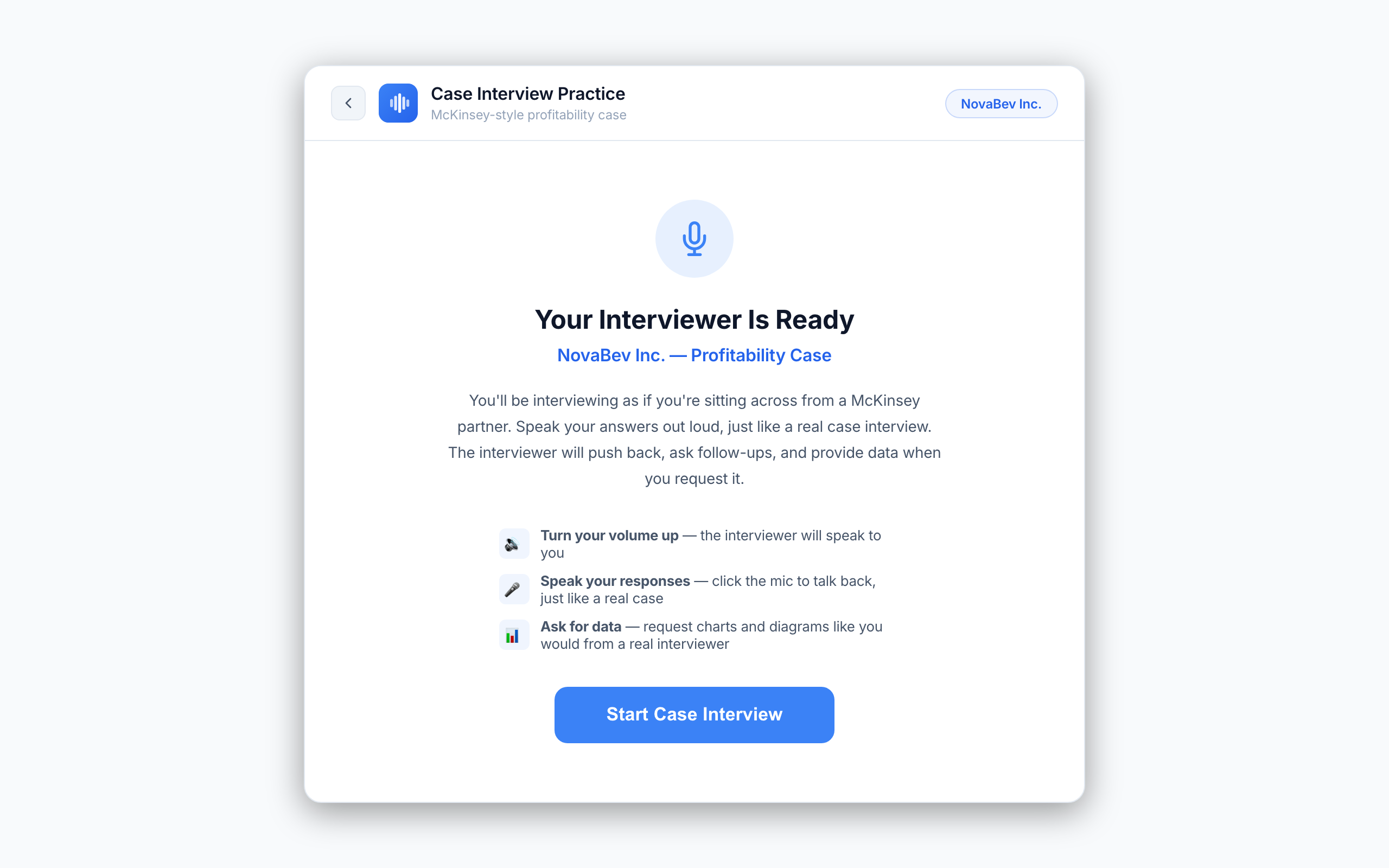

The AI Interviewer Pushes Back

Caise’s AI interviewer uses Socratic pushback, which means it will not let you get away with surface-level answers. If you say “revenue is down,” expect an immediate follow-up: “Which segment? By how much? Since when?” If you say “costs are increasing,” the interviewer will push: “Fixed or variable? What is the largest cost line item? Has the cost structure changed, or has volume changed?” This is exactly how real MBB interviewers operate, and it forces you to think precisely rather than vaguely.

Live Handouts and Exhibits

When you ask the right questions during a Caise case – say you request a cost breakdown or ask to see revenue by segment – the AI may share an interactive handout or exhibit for you to analyze in real time. You might receive a table showing COGS, SG&A, and overhead trends over three years, or a chart breaking revenue into product lines by quarter. You need to interpret the data, spot the anomaly, and weave it into your hypothesis – just like you would in a live interview when the interviewer slides a page across the table.

What Each Dimension Measures

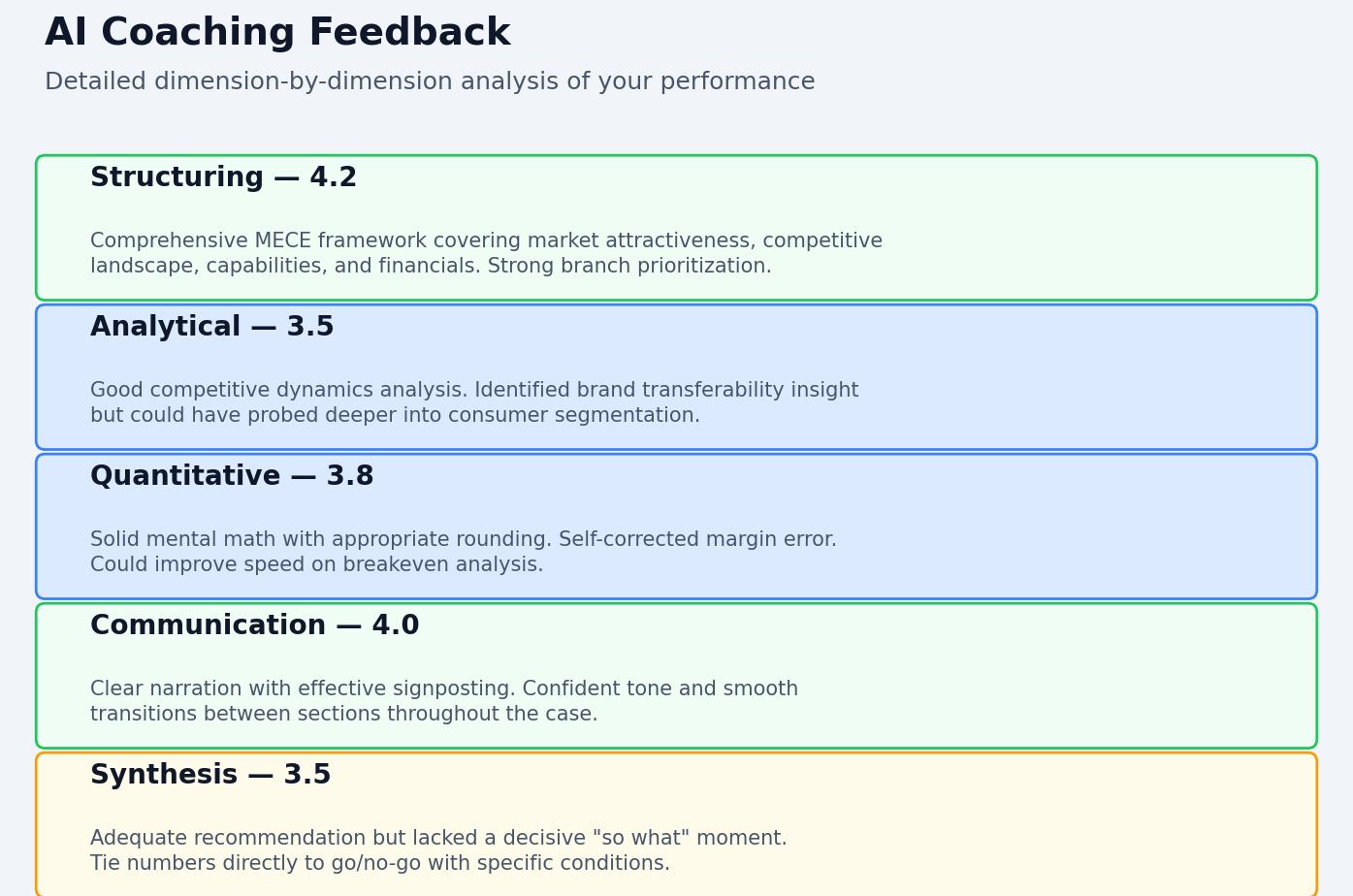

Caise evaluates every case on five dimensions, each scored 1 to 5. Two of them are especially critical in profitability cases:

- Quantitative: Can you correctly decompose Profit = Revenue - Costs? Do you structure your calculations before computing? Do you sanity-check your results against the context of the case? Candidates who get a number and move on without asking “does this make sense?” lose points here.

- Analytical: Are you asking targeted questions to test specific hypotheses, or are you fishing with generic questions hoping the interviewer hands you the answer? Strong analytical performance means each question you ask eliminates a branch of the issue tree or confirms a hypothesis.

The other three dimensions – Structuring, Communication, and Synthesis – round out the picture. Structuring tests whether you laid out a clear, MECE framework upfront. Communication tests whether you signposted your approach and kept the interviewer oriented. Synthesis tests whether your final recommendation tied back to the data and told a coherent story.

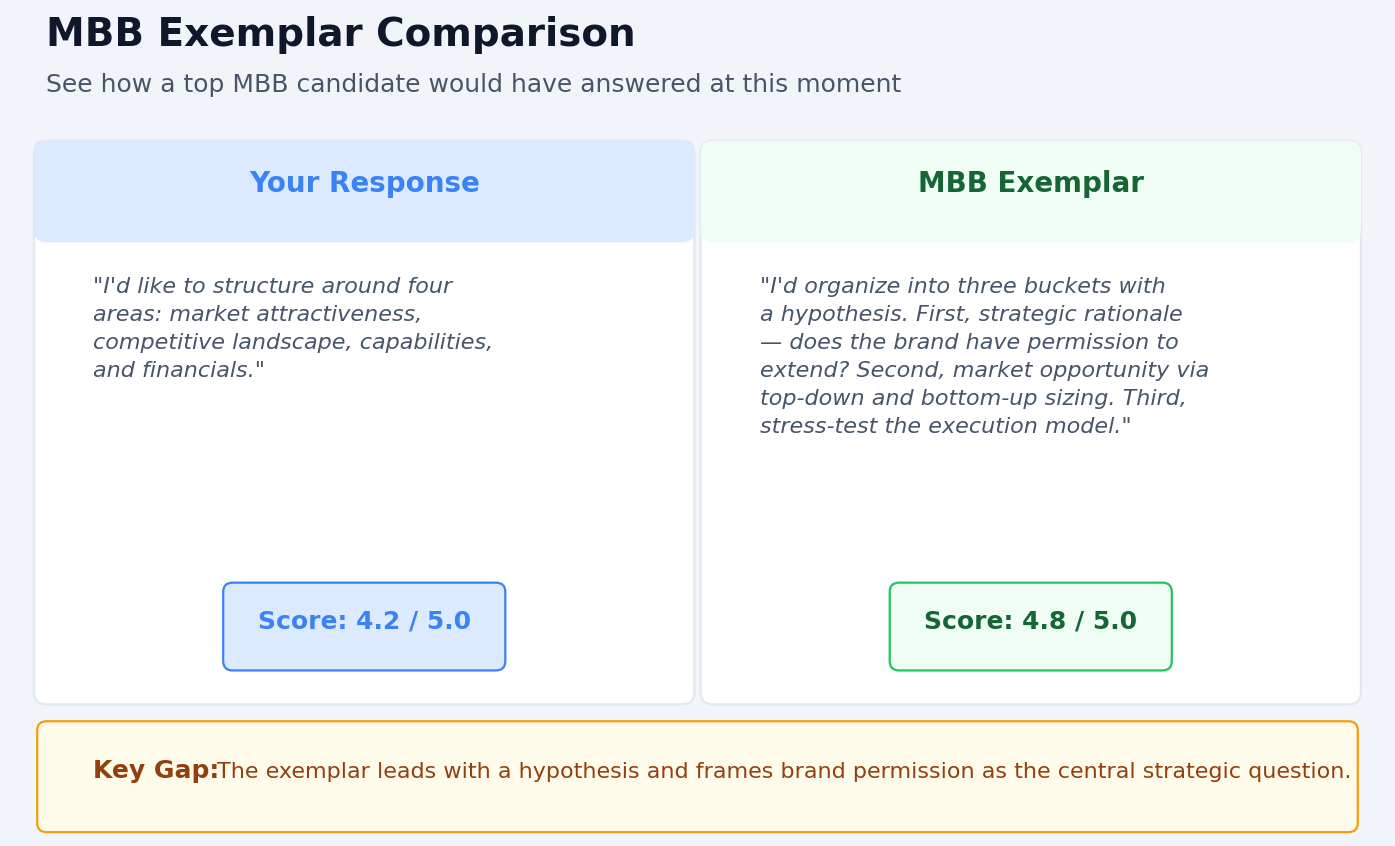

MBB Exemplar Responses

After every case, Caise shows you MBB Exemplar responses at your weakest moments. If you stumbled during the cost analysis, you will see exactly what a Distinctive-rated candidate would have said in that same spot – the specific words, the structure, the level of quantitative detail. This is not generic advice. It is a direct comparison between your response and the bar you need to clear.

Score Progression Over Time

Caise tracks your scores across every case you complete. Over weeks of practice, you can see your profitability case scores on a radar chart, broken down by dimension, improving session by session. If your Quantitative scores are consistently lagging while your Structuring scores are strong, you know exactly where to focus your next practice session.

Practice Makes Permanent

The key to profitability cases is repetition. After doing 20 or 30 of them, the diagnostic pattern becomes instinctive. You will start hearing the case prompt and immediately forming hypotheses about what is driving the margin decline. That speed and confidence is exactly what interviewers are looking for.

Caise is built for this kind of deliberate repetition. Every case is voice-based – you speak your answers out loud, just like in a real interview. This matters because profitability cases require you to think and communicate simultaneously. Reading a framework off a page is easy. Articulating a structured cost decomposition while doing mental math in front of an interviewer is a completely different skill, and it only develops through verbal practice.

After each case, Caise runs a debrief session where you can ask the AI coach follow-up questions about your performance. “Why did I lose points on Synthesis?” “What should I have done differently when I got the cost exhibit?” “Was my recommendation too vague?” The coach walks you through your specific weaknesses with concrete examples from the case you just completed.

Over multiple cases, Caise’s coaching insights identify recurring patterns in your performance. Maybe you consistently rush past the revenue segmentation step. Maybe your math is strong but you forget to sanity-check results. Maybe you structure well but your final synthesis never ties back to the original question. These patterns are invisible when you practice alone or with a study partner, but they are exactly the habits that determine your score on interview day.

Profitability cases are the single most common case type you will face. Start practicing on Caise now – pick from 60+ real MBB and HBS cases, get scored on five dimensions after every case, and see exactly where you stand against the Distinctive bar. Your first case takes 15 minutes.